By [Jawad Shah] – Finance & Expense Automation Specialist

Managing personal finance effectively starts with understanding where money goes each month. Monthly expenses represent all recurring costs individuals or households pay regularly, from fixed bills like rent to variable spending on groceries and entertainment. Tracking these costs provides financial awareness and helps prevent overspending, yet many people overlook dozens of charges that quietly drain their accounts.

What Are Monthly Expenses? (Definition & Why They Matter)

Monthly expenses encompass every payment made within 30 days. This includes everything from recurring monthly bills like utilities to discretionary spending on hobbies. Understanding what counts as monthly expenses helps create realistic budgets and improve cash flow management.

The importance of monitoring these costs cannot be overstated. When individuals track monthly expenses consistently, they gain clarity about their spending habits and can identify opportunities to reduce monthly expenses. This financial discipline transforms vague notions about money into actionable data that supports better decisions.

Fixed vs. Variable Monthly Expenses Explained

Fixed expenses remain constant each billing cycle. These predictable costs include:

- Rent or mortgage payments

- Car loan payments

- Insurance premiums

- Subscription payments for services

Variable expenses fluctuate based on usage and choices:

- Grocery and food spending

- Utility costs (electricity, water)

- Transportation expenses (fuel, parking)

- Entertainment and dining out

An expense that costs the same every month falls into the fixed category, making budget planning easier. Variable costs require closer monitoring since they respond to behavioral changes and seasonal factors.

How Monthly Expenses Impact Your Financial Health

The relationship between income and expenses determines financial stability. When monthly expenses consume too much income, savings suffer, and debt accumulates. A healthy monthly expense breakdown typically allocates funds across essential categories while maintaining room for savings and emergency fund contributions.

Poor expense monitoring leads to common problems: depleted checking accounts before the month’s end, reliance on credit cards, and inability to handle unexpected costs. Conversely, effective monthly expense management creates breathing room in budgets, reduces financial stress, and enables progress toward long-term goals.

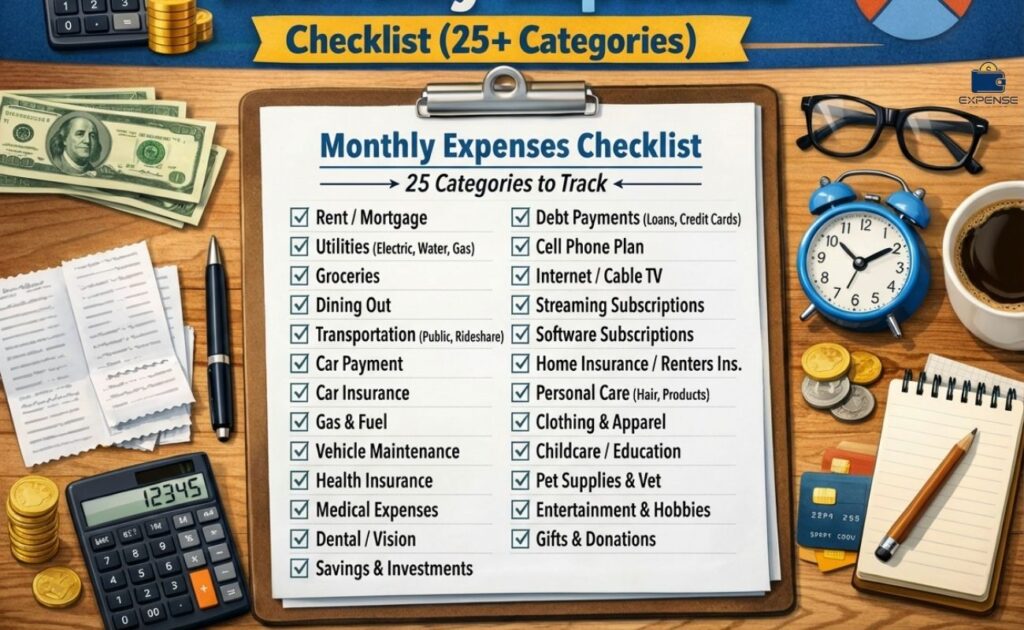

Complete Monthly Expenses Checklist (25+ Categories)

A comprehensive monthly expenses list captures every area where money flows out. This checklist serves as a foundation for building a complete personal monthly expenses tracker.

Housing & Living Expenses

Housing represents the largest category for most households. Common monthly expenses in this area include:

- Rent or mortgage payments

- Property taxes (often collected monthly through escrow)

- HOA fees for condominiums and planned communities

- Home maintenance reserves for repairs and upkeep

- Renter’s or homeowner’s insurance

Utilities & Essential Services

These recurring monthly bills keep households functioning:

- Electricity

- Water and sewer

- Natural gas or heating oil

- Internet service

- Phone service (mobile and landline)

- Waste management and recycling

Transportation Costs

Getting around generates multiple expense categories:

- Car loan or lease payments

- Fuel costs

- Auto insurance

- Regular maintenance (oil changes, tire rotations)

- Public transit passes

- Ride-sharing services

- Parking fees

Food & Dining

Grocery expenses per month vary widely by household size and eating habits. This category includes:

- Groceries and household supplies

- Meal delivery services

- Dining out at restaurants

- Coffee shop purchases

- Meal prep ingredients

Insurance Premiums

Protection costs add up across multiple policies:

- Health insurance

- Dental and vision coverage

- Life insurance

- Disability insurance

- Auto insurance

- Home or renter’s insurance

- Umbrella liability policies

Debt Obligations

Monthly payments on borrowed money include:

- Credit card minimum payments

- Student loan payments

- Personal loan installments

- Medical debt payments

Savings & Investments

Building wealth requires treating savings as non-negotiable monthly expenses:

- Emergency fund contributions

- Retirement account deposits (401k, IRA)

- Investment portfolio additions

- Sinking funds for planned purchases

Healthcare & Wellness

Beyond insurance premiums, health costs include:

- Out-of-pocket medical expenses

- Prescription medications

- Therapy or counseling sessions

- Fitness memberships

- Preventive care copays

Family & Dependent Care

Households with dependents face additional typical monthly expenses:

- Childcare or daycare

- School tuition and fees

- Children’s extracurricular activities

- Elder care services

- Child support or alimony payments

For reference, average monthly expenses for a family of 4 significantly exceed single-person costs, often ranging from $5,000 to $8,000 depending on location and lifestyle.

Pet Care Expenses

Animal companions require dedicated budget allocation:

- Pet food and treats

- Veterinary care and medications

- Grooming services

- Pet insurance

- Supplies and toys

Personal Care & Clothing

Maintaining appearance involves regular costs:

- Haircuts and styling

- Toiletries and personal hygiene products

- Clothing purchases and replacements

- Dry cleaning services

- Personal grooming (nails, skincare)

Entertainment & Leisure

Discretionary spending on enjoyment includes:

- Streaming service subscriptions

- Hobby supplies and equipment

- Concert or event tickets

- Travel and vacation expenses

- Dining experiences

Subscriptions & Memberships

Digital age living generates numerous subscription payments:

- Streaming platforms (Netflix, Spotify, etc.)

- Professional association dues

- Club memberships

- Software licenses

- Cloud storage services

Technology & Communication

Staying connected requires ongoing investment:

- Smartphone payment plans

- Software subscriptions

- Cloud storage fees

- Technology upgrades and replacements

Professional & Career Expenses

Career advancement sometimes requires a monthly investment:

- Continuing education courses

- Professional development programs

- Networking event fees

- Work supplies and equipment

Charitable Giving & Personal Values

Many individuals budget for contributions:

- Charitable donations

- Religious tithing

- Community support initiatives

Monthly Expenses Hidden Costs People Often Forget

Creating an accurate list of monthly expenses requires identifying charges that slip through cracks. These overlooked items create budget gaps that lead to month-end shortfalls.

Annual Fees Broken Down Monthly

Services with yearly billing deserve a monthly allocation. Examples include:

- Amazon Prime membership ($139 annually = ~$12 monthly)

- Costco or Sam’s Club membership

- Professional licenses and certifications

- Website hosting and domain registration

- Software annual subscriptions

Smart budgeters divide annual costs by 12 and include them in monthly expense categories.

Irregular Expenses That Sneak Up

Semi-regular costs catch people off guard:

- Birthday and holiday gifts

- Vehicle registration and inspection

- Quarterly estimated taxes (for self-employed individuals)

- Semi-annual insurance payments

- Seasonal clothing needs

Subscription Creep: The Silent Budget Killer

Free trials turn into forgotten subscription payments. The average household carries 10-15 active subscriptions, many unused. Regular subscription audits prevent this expense monitoring blind spot.

Seasonal Expense Variations

Certain costs fluctuate predictably:

- Summer utility costs (air conditioning)

- Winter heating expenses

- Holiday spending surges

- Back-to-school shopping

- Vacation season travel

Average Monthly Expenses in 2026: How Do You Compare?

Understanding benchmarks helps evaluate personal spending patterns.

National Average Breakdown by Category

| Expense Category | Average Monthly Amount | Percentage of Budget |

| Housing | $1,784 | 33% |

| Transportation | $819 | 15% |

| Food | $779 | 14% |

| Insurance & Pensions | $724 | 13% |

| Healthcare | $414 | 8% |

| Entertainment | $268 | 5% |

| Other Expenses | $646 | 12% |

| Total | $5,434 | 100% |

These figures represent typical monthly expenses for average American households, though individual circumstances vary significantly.

Monthly Expenses by Age Group & Life Stage

Financial obligations shift across life phases:

- Young professionals (22-35): Average $3,800-$4,500 monthly, higher discretionary spending

- Families with children (35-55): Average $6,000-$8,500 monthly, with elevated childcare and education costs

- Empty nesters (55-65): Average $5,000-$6,500 monthly, reduced family expenses, but increased healthcare costs

- Retirees (65+): Average monthly retirement expenses around $4,000-$5,000, with healthcare comprising a larger portion

Single vs. Family Monthly Expense Benchmarks

Household size dramatically affects spending:

Single individuals: $2,500-$3,500 monthly, Couples without children: $4,000-$5,500 monthly

Family of four: $6,000-$8,500 monthly

Cost of Living Adjustments by Region

Geographic location creates vast expense differences. For instance, the cost of living in Switzerland, including monthly expenses, often exceeds $5,000-$7,000 per person due to high housing and service costs. Conversely, rural American areas might see household monthly expenses at 40-60% of urban coastal city levels.

How to Calculate Your Total Monthly Expenses (Step-by-Step)

Accurate calculation requires a systematic approach. This budget planning process works for beginners and experienced budgeters alike.

Step 1: Gather All Financial Statements (Past 3 Months)

Collect bank statements, credit card bills, and receipts from the previous quarter. Three months of data reveal patterns that single-month snapshots miss.

Step 2: Categorize Every Transaction

Sort each expense into athe ppropriate monthly expense categories. Digital tools simplify this process, but manual categorization using a monthly expenses sheet builds deeper financial awareness.

Step 3: Identify Fixed and Variable Expenses

Mark which costs stay constant (fixed) versus those that fluctuate (variable). This distinction enables more strategic control of monthly spending efforts.

Step 4: Calculate Category Averages

Add each category’s three-month total and divide by three. This average monthly expenses figure smooths out irregularities and provides realistic planning numbers.

Step 5: Add Hidden & Annual Costs (Prorated Monthly)

Include overlooked items identified earlier. Divide annual expenses by 12 to create monthly amounts.

Step 6: Compare Against Your Income

Calculate total monthly expenses and compare to monthly income. The resulting number shows whether spending aligns with earnings or creates deficit situations requiring adjustment.

Best Methods for Tracking Monthly Expenses

Different money management systems suit different personalities and situations. Understanding how to track monthly expenses easily involves finding the right approach.

The Envelope System (Digital & Physical)

This cash-based method allocates monthly income into category-specific envelopes. When an envelope empties, spending in that category stops until the next month. Digital versions use virtual envelopes while maintaining the same spending control principle.

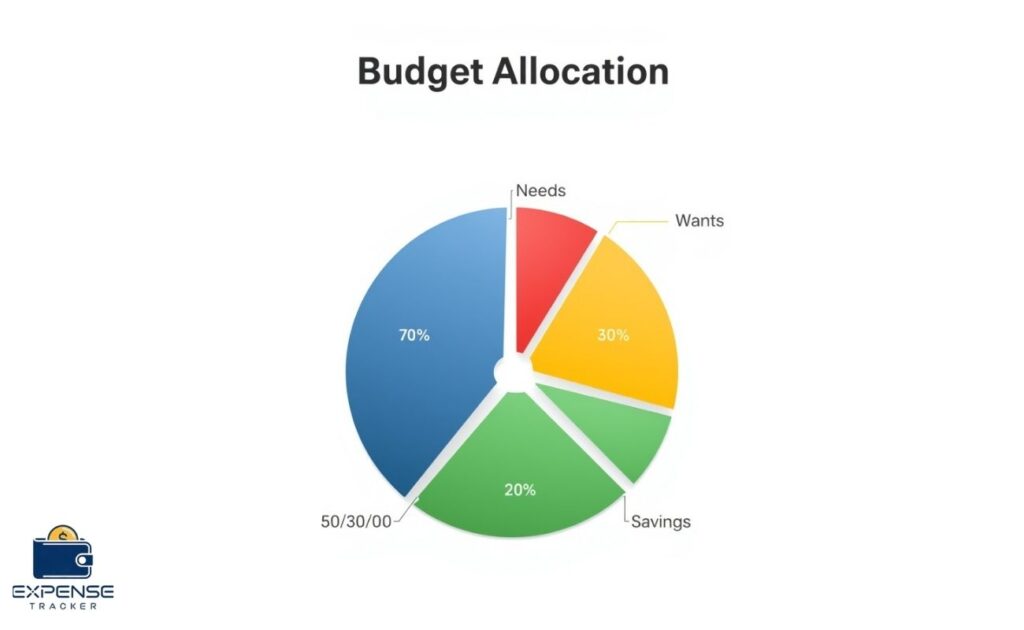

50/30/20 Budgeting Rule

This popular framework divides after-tax income:

- 50% for needs (housing, utilities, groceries)

- 30% for wants (entertainment, dining out)

- 20% for savings and debt repayment

Zero-Based Budgeting Method

Every dollar receives an assignment before the month begins. Income minus all planned expenses and savings equals zero, ensuring complete monthly expense management without unallocated funds.

Pay Yourself First Strategy

Automatic transfers to savings occur immediately upon income receipt. Remaining funds cover monthly expenses, forcing spending habits analysis and adjustment.

Which Method Works Best for Your Situation?

Consider these factors when selecting a system:

- Time availability: Zero-based budgeting requires more setup than 50/30/20

- Income stability: Variable income earners benefit from envelope systems

- Financial goals: Aggressive savers prefer Pay Yourself First

- Personality type: Detail-oriented individuals thrive with zero-based approaches

Top Tools for Managing Monthly Expenses

Technology transforms expense monitoring from a tedious chore to an automated insight generator.

Expense Tracker Spreadsheets & Templates (Free Download)

For those comfortable with Excel or Google Sheets, the monthly expenses template Excel files provide customizable solutions. These monthly expenses spreadsheet options offer flexibility without subscription costs.

Best Budgeting Apps Reviewed (Mint, YNAB, PocketGuard)

Modern apps sync with bank accounts, categorize transactions automatically, and provide real-time spending alerts:

- Mint: Free, comprehensive monthly expense tracker tool

- YNAB (You Need A Budget): Subscription-based, zero-based budgeting focus

- PocketGuard: Simplified interface showing available spending money

How ExpenseTrackerTool.com Simplifies Monthly Expense Management

This monthly expenses tracker tool offers user-friendly interfaces designed specifically for comprehensive expense categorization. The platform combines spreadsheet flexibility with app convenience, enabling users to track monthly expenses without complex setup.

Bank-Integrated Tracking vs. Manual Entry

Automatic bank connections save time but may miss cash transactions. Manual entry requires more effort but ensures complete accuracy. Hybrid approaches often deliver optimal results.

Smart Strategies to Reduce Monthly Expenses

Understanding current spending enables strategic reduction efforts. These tactics help control monthly spending without drastically reducing quality of life.

The 10 Easiest Expenses to Cut Without Lifestyle Impact

- Cancel unused subscriptions

- Reduce dining out frequency by one meal weekly

- Make coffee at home instead of buying it daily

- Lower the thermostat by 2 degrees in winter

- Switch to LED bulbs

- Eliminate bank fees through proper account management

- Use library resources instead of purchasing books

- Prepare larger meal batches to reduce cooking frequency

- Bundle insurance policies for discounts

- Negotiate lower interest rates on credit cards

Negotiation Scripts for Lowering Bills (Internet, Insurance, etc.)

Service providers often reduce rates when customers request discounts. Simple script: “I’ve been a loyal customer for [X] years. My budget is tight right now. What promotions or discounts can you offer to help me reduce this bill?”

Subscription Audit: Cancel What You Don’t Use

Review all subscription payments monthly. Ask: “Did I use this service in the past 30 days?” If not, cancel immediately. Most services allow easy reactivation if later needed.

Energy Efficiency Hacks That Lower Utility Bills

- Program thermostats for automatic temperature adjustments

- Seal window and door gaps

- Run full loads in dishwashers and washing machines

- Unplug devices when not in use

- Use natural light during daytime hours

Transportation Cost Reduction Strategies

- Combine errands into single trips

- Maintain proper tire pressure

- Use public transit when practical

- Carpool for regular commutes

- Consider cycling for nearby destinations

Food Budget Optimization Without Sacrifice

- Create weekly meal plans

- Shop with lists to avoid impulse purchases

- Buy generic brands for staples

- Prepare lunches instead of buying

- Use cashback apps at grocery stores

Monthly Expense Planning for Different Life Situations

Effective household budgeting adapts to individual circumstances.

Monthly Budgeting for Single Professionals

Focus areas include building emergency funds, maximizing retirement contributions, and balancing career investment with lifestyle enjoyment. Personal monthly expenses typically range from $2,500 to $4,000.

Couple’s Expense Management Strategy

Shared household monthly expenses require communication about financial priorities, combined or separate accounts, and equitable contribution systems based on income proportions.

Family Monthly Budget with Children

Childcare, education, and activity costs demand careful planning. The monthly expenses of a family increase substantially, requiring a detailed monthly expense breakdown across numerous categories.

Retirement Planning: Fixed Income Expense Management

Retirees face what is the average monthly retirement expenses while managing healthcare costs and potential inflation. Conservative spending and healthcare cost planning become priorities.

Student Budget: Managing Expenses on Limited Income

Students benefit from monthly expenses for beginner guidance, focusing on essentials while minimizing debt accumulation through careful discretionary spending control.

Common Monthly Expense Tracking Mistakes (& How to Fix Them)

Even dedicated budgeters fall into predictable traps that undermine their efforts.

Underestimating Variable Expenses

Many people use best-case scenarios for variable costs. Solution: Use three-month averages instead of wishful thinking when creating monthly expenses planner documents.

Forgetting to Budget for Fun (Leads to Budget Failure)

Overly restrictive budgets trigger rebellion and abandonment. Solution: Include reasonable entertainment allowances in the monthly expense summary.

Not Accounting for Income Fluctuations

Freelancers and commission-based workers need flexible systems. Solution: Base monthly expenses on minimum expected income, treating higher months as savings opportunities.

Over-Complicated Tracking Systems

Elaborate monthly business expense template setups often get abandoned. Solution: Start simple with basic categories, adding complexity only when necessary.

Ignoring Small Recurring Charges

$5 monthly subscriptions seem insignificant, but accumulate substantially. Solution: Track every charge regardless of size in the monthly expense report.

Creating Your Personalized Monthly Expense Budget

Building sustainable financial habits follows a progression that improves over time.

Month 1: Tracking & Awareness Phase

Focus exclusively on recording every expense without judgment or restriction. This baseline data reveals true spending habits and identifies all monthly expense categories currently in use.

Month 2: Analysis & Adjustment Phase

Review Month 1 data, identify reduction opportunities, and set realistic targets. Create a monthly expenses list pdf or digital version showing planned allocations.

Month 3: Optimization & Automation Phase

Implement automatic savings transfers, bill payment automation, and refine category allocations based on Month 2 performance. The money management system starts becoming habitual.

Ongoing: Monthly Budget Review Checklist

- Compare actual versus planned spending

- Adjust category allocations as needed

- Celebrate wins and identify improvement areas

- Update financial goals based on progress

Monthly Expense Tracking Resources & Next Steps

Taking control of personal finance begins with implementing systems that match individual needs and preferences. The monthly expenses meaning extends beyond simple record-keeping—it represents a commitment to financial discipline and awareness that transforms economic futures.

Successful expense monitoring creates a foundation for achieving financial goals, from building emergency funds to planning major purchases. By understanding the monthly expenses in business or household contexts, individuals gain power over their money rather than feeling controlled by it.

Start today by selecting a tracking method, whether a digital monthly expense tracking app, a downloadable monthly expenses list template, or a simple monthly expense calculator online. The key lies not in perfect execution from day one, but in consistent effort that builds financial habits and analysis capabilities over time.

Remember that monthly expense management represents an ongoing journey rather than a destination. Regular review, honest assessment, and willingness to adjust strategies ensure systems remain effective as life circumstances evolve. The investment of time and attention pays dividends through reduced financial stress, increased savings capacity, and clearer paths toward long-term financial objectives.

Conclusion

Mastering monthly expense management transforms financial stress into financial confidence. Whether tracking household monthly expenses through a simple monthly expenses list template or utilizing sophisticated online monthly expenses tools, the path to financial stability begins with awareness and consistent monitoring. Understanding monthly expense categories—from fixed housing costs to variable entertainment spending—empowers individuals to make informed decisions that align spending with values and goals. The journey from financial confusion to clarity doesn’t require perfection; it requires commitment to tracking, analyzing, and adjusting spending patterns over time.

For those seeking a straightforward solution, ExpenseTrackerTool.com offers a free monthly expense tracker designed specifically to simplify this process. Unlike complicated spreadsheets or overwhelming financial software, this online monthly expenses tool provides intuitive categorization, visual spending breakdowns, and actionable insights that help users identify saving opportunities within minutes.

The platform combines the flexibility of manual tracking with the convenience of automated categorization, making it an ideal choice for anyone from budgeting beginners to seasoned financial planners looking to streamline their monthly expense management system.

Taking control of personal finances starts with a single decision: to know where money goes each month. By implementing the strategies outlined in this guide and leveraging the right tools, anyone can build sustainable financial habits that lead to reduced debt, increased savings, and greater peace of mind. Start tracking today, review progress regularly, and watch as small, consistent efforts compound into significant financial improvements that reshape your economic future.

FAQs

Q: What are monthly expenses?

A: Monthly expenses include all money spent during 30 days, from fixed bills to variable purchases across housing, food, transportation, and personal categories.

Q: What should be my monthly expenses?

A: Ideal total depends on income and location. As a guideline, aim for monthly expenses at or below 80% of after-tax income, allowing 20% for savings and debt reduction.

Q: What are the top 3 expenses?

A: For most households, housing (rent/mortgage), transportation (car payments/fuel), and food (groceries/dining) consume the largest budget portions.

Q: What are 10 examples of expenses?

A: Common examples include rent, utilities, groceries, car payments, insurance, phone service, streaming subscriptions, healthcare, clothing, and entertainment.

Q: How much should monthly expenses be?

A: This varies by income, but the 50/30/20 rule suggests 50% of income for needs, 30% for wants, leaving 20% for savings. A household earning $5,000 monthly might allocate $2,500 for needs, $1,500 for wants, and $1,000 for savings.

Q: What counts as monthly expenses?

A: Any predictable or variable cost occurring within the billing cycle counts, including fixed bills, variable purchases, and prorated annual costs divided by 12.

Q: How do I track monthly expenses easily?

A: The simple way to track monthly expenses involves choosing one method (app, spreadsheet, or envelope system) and consistently recording all spending immediately when it occurs.

Q: What is the best way to manage monthly expenses?

A: Best practices combine automated tracking tools, regular review schedules, realistic category allocations, and adjustment flexibility as circumstances change.

Q: Why is tracking monthly expenses important?

A: Tracking creates financial awareness, prevents overspending, identifies saving opportunities, and provides data for informed financial decisions.

Q: Can monthly expenses be tracked automatically?

A: Yes, expense tracking software and budgeting apps sync with bank accounts and credit cards, automatically categorizing most transactions while allowing manual adjustment for accuracy.

Q: How much does final expense insurance cost per month?

A: Final expense insurance typically costs $30-$70 monthly for modest coverage amounts, varying by age, health status, and benefit amount selected.

Finance & Expense Automation Specialist With 3 years of experience.